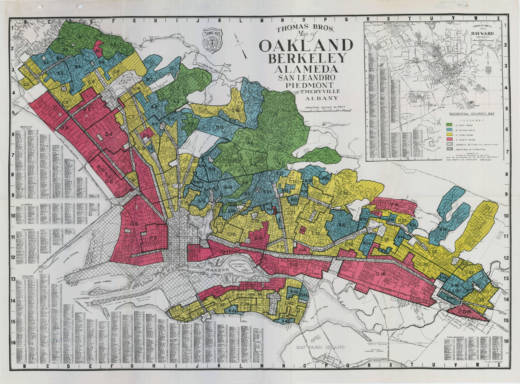

A 1937 Oakland and Berkeley "residential security map" created by the Home Owners' Loan Corporation. (Courtesy of University of Maryland's T-RACES project)

The Trump administration has made it a priority to roll back government regulations, on everything from the environment to the internet. One target for reform is the Community Reinvestment Act, or CRA, a 40-year-old law designed to get banks to invest in low-income communities and help them recover from the negative effects of redlining.

"It may be one of the most impactful laws people have never heard of," says Kevin Stein, deputy director of the California Reinvestment Coalition.

Recovering from Redlining in Oakland's Fruitvale. Has The Community Reinvestment Act Helped?

Stein estimates that, nationwide, the CRA has resulted in billions of dollars of loans, investments and financial services for low-income communities and communities of color.

To really understand the impact of the Community Reinvestment Act, it helps to know why it became law in the first place. It all goes back to the practice that came to be known as redlining.

In the 1930s, as the country was recovering from the Great Depression, the federal government wanted to encourage homeownership in cities that had suffered from waves of foreclosures. So it established the Home Owners' Loan Corporation (HOLC), to refinance mortgages at risk of default. As part of that effort, HOLC created maps of cities, to identify which neighborhoods were good investments and which were bad investments.

Sponsored

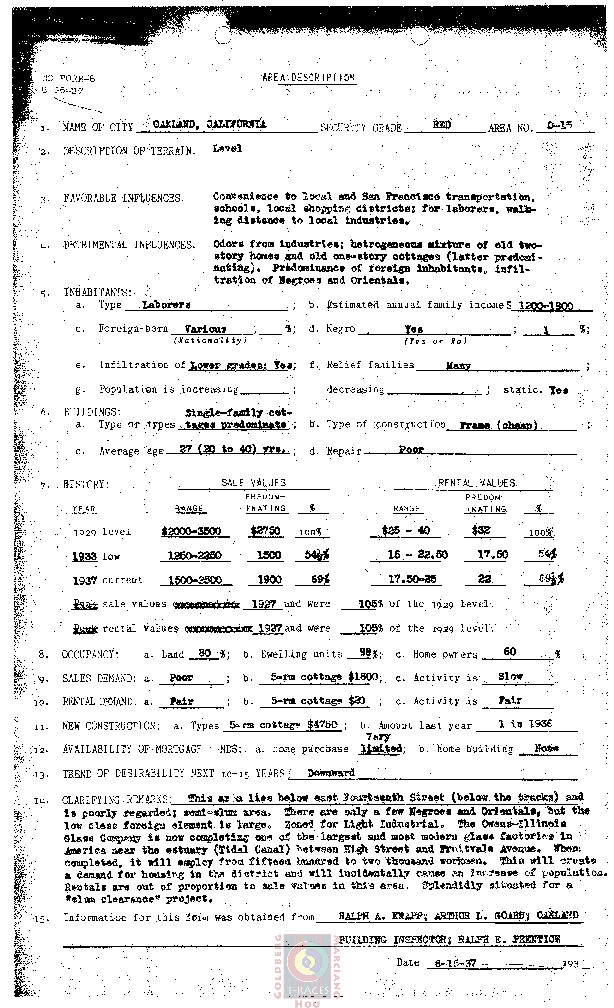

HOLC assigned each neighborhood a grade, according to the "favorable" and "detrimental" influences in the neighborhood. The presence of minority communities was among the so-called detrimental influences. Take Oakland's Fruitvale neighborhood, for instance. A 1937 HOLC map of the area indicated these so-called detrimental influences: "Odors from industries. Predominance of foreign inhabitants. Infiltration of Negroes and Orientals."

An "area description" of an Oakland neighborhood, produced by the Home Owners' Loan Corporation in 1937. (Courtesy of the University of Maryland T-RACES project)

Fruitvale and other neighborhoods given low grades were colored red on the maps, which spawned the term "redlining."

"These neighborhoods were denied access to credit because the federal government refused to guarantee mortgages and other loans that were being made in these neighborhoods," said Carolina Reid, an assistant professor of city and regional planning at UC Berkeley.

That, said Reid, had a profound and lasting impact. "The policy of redlining helped facilitate the disinvestment and the growing poverty in neighborhoods like Fruitvale," Reid said. "Because we saw white flight to the suburbs and then we saw families that were remaining not being able to access credit to buy a home or to invest in a small business."

In the 1960s and '70s, activists raged about the decline of cities and the influence of discriminatory lending practices. That led to the passage of a number of laws, including the Community Reinvestment Act in 1977.

The CRA doesn't specifically outlaw redlining or discrimination against borrowers on the basis of race. Instead, it mandates that banks offer loans and other financial services to all communities where they do business, including low- and moderate-income areas.

As part of the CRA, banks are encouraged to work with local community groups to find opportunities for loans or investments that can actually help a struggling community. In Oakland, the nonprofit Unity Council has taken on that role. With investment from banks, the Unity Council built Fruitvale Village, the transit village next to the Fruitvale BART Station. It includes 47 units of housing, restaurants, businesses and a bank branch.

As part of investing in projects like Fruitvale Village, banks get credit for complying with the Community Reinvestment Act. And because of CRA, banks now see places like Fruitvale as good investments, says Chris Iglesias, CEO of the Unity Council.

"It wasn't necessarily out of the goodness of their heart. But I think this has become a much more viable option for them, under this program, and we've taken advantage of that," Iglesias said.

Investment from banks didn't just help build Fruitvale Village. It helps the Unity Council fund community services for people who live in the neighborhood, like a health clinic, job training and Head Start.

Silvia Guzman's three kids came through the Head Start program. She first learned about it when she was just 16 years old, with a young daughter at home. A family advocate approached her mother after church one Sunday.

"My mom came home and she told me, and I said I don't think we need child care," Guzman recalled recently while standing outside the Head Start classroom. "And she says, 'No honey, this is not child care. You know, this is school-oriented. They will teach her, they will guide her, she will learn her numbers, she will learn how to write.' "

Silvia Guzman serves on the board of the Unity Council, a Community Development Corporation that built Fruitvale Village in Oakland. (Brian Watt/KQED)

She enrolled her daughter, Gloria, in Head Start. When she did, she sat down with a program staffer, who helped her build goals for herself as well. Guzman now serves on the board of the Unity Council, and educates other parents in the neighborhood.

"This is my roots, and this is where my children played," she said. "And this is where my children get their education and their services are met, and I shouldn't have to go anywhere else if I have that at home."

So for people like Silvia Guzman, and places like Fruitvale, the Community Reinvestment Act has made a difference. But it's not perfect.

Discriminatory lending practices have not become a thing of the distant past. And as Oakland and the Bay Area struggle with an epic shortage of affordable housing, advocates say that banks can and should be doing more to help.

Stein, with the California Reinvestment Coalition, thinks that banks should be taking more creative approaches to helping people stay in their homes.

"Perhaps do more to work with nonprofits to buy buildings at risk of being flipped due to market pressures," Stein suggests. "So that people who have been living in the Bay Area for a long time can continue to live in the Bay Area, because when people get evicted you know it's very hard for them to find places to go."

In addition to giving credit to banks for their beneficial investments and loans, Stein argues the Community Reinvestment Act could be tougher, and penalize banks more for what he calls "bad behavior," like making loans to real estate investors who purchase buildings and then evict longtime tenants.

Wells Fargo recently had their CRA score downgraded, in part because of the scandal where the bank opened thousands of unauthorized accounts in customers' names.

But with the Trump administration's preference for deregulation, the California Reinvestment Coalition and other groups are anxiously waiting to see what comes next.

The Treasury Department and the Office of the Comptroller of the Currency, which both oversee compliance with the CRA, have said they plan to unveil proposals for changes in the coming months. This wouldn't be the first time the CRA has been modified in its history.

"We're expecting that there will be efforts to dilute and weaken the CRA and its impacts on the community, and we are getting ready to fight them," Stein said.

Meanwhile, in Oakland, phase two of the Fruitvale Village project is getting underway, again with major investments from banks. This time there is a major focus on affordable housing. Of 275 rental units, 94 will be affordable family homes and 20 will be reserved for formerly homeless veterans.

lower waypoint

Stay in touch. Sign up for our daily newsletter.

To learn more about how we use your information, please read our privacy policy.

window.__IS_SSR__=true