We are wrapping up the first phase of our PriceCheck project. The goal is to shine a light on costs of common health care procedures in California. We're starting with screening mammograms, and already we've found that the cash price (for people who are uninsured or have gone out of network) varies from a low of $60 at the H. Claude Hudson Comprehensive Health Center in Los Angeles, a county-run clinic, to $801 at U.C. San Francisco on the high end.

In order to do that, you need to get familiar with your insurance company's "explanation of benefits" or EOB. That's the form your insurer sends to explain what was paid, to whom, at what level and why.

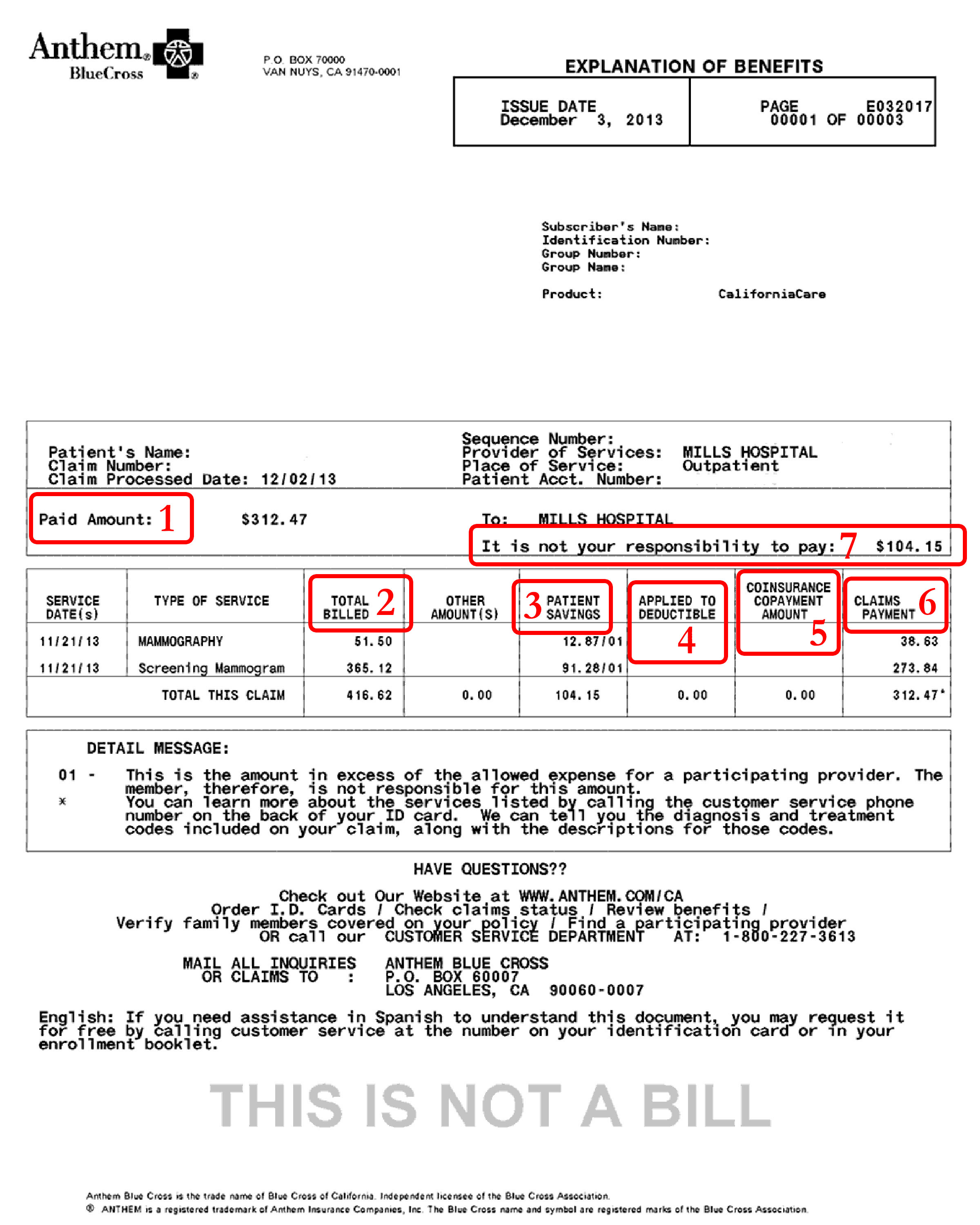

Here's a typical EOB, that we've marked with some explanations below:

An explanation of benefits from Anthem Blue Cross.

The information included on an EOB isn’t consistent from one health care insurance company to the next, Palmer says, and they often include abbreviations and other language difficult for the average consumer to understand.

We've numbered items above and here are the descriptions of each:

1. "Paid Amount." This is the total amount of money that the insurance company has paid directly to the provider, Palmer says. Or, in an out-of-network situation, it may be paid to the member. If you scan farther across that line to the right, you’ll see who the insurance company paid; in this case, it’s Mills Hospital.

2. "Total Billed." These are the amounts being billed to the insurance company by the provider for each service — in this case, $51.50 for mammography (likely what the physician was paid to interpret the mammogram, although it does not say) and $365.12 for the screening mammogram (likely the facility fee for the patient to have the mammogram done, although it does not say). The charges are then totaled below the line.

In addition to an EOB, individuals will usually receive an itemized bill from their provider(s). Palmer says it’s important to be sure the total billed amount on the EOB — in this case, $416.62 — matches the total billed amount on the itemized bill from the provider.

3. "Patient Savings." This is the difference between what the provider charged for this service and the amount they agreed to accept as a participating provider of your health insurance plan. That's because when a doctor or other provider agrees to contract with an insurer, they agree to accept reimbursement at a lower price than the charged price. In American medicine, the amounts charged by providers generally bear little relation to what they are ultimately paid.

There should always be a code that identifies the reason for the savings, Palmer says. And although it’s a little hard to see, there is a “01” that follows each charge in this column — that “01” corresponds to the “detail message” in the box below. “It’s usually clearer than that,” Palmer says, adding that consumers reading this EOB may miss that little “01” mark after the charge. “It’s usually a separate column that says ‘remark’ or ‘reason,’ and they’ll put the ‘01’ in there.”

In this case, Palmer says the “01” remark indicates that the provider billed more than was allowed under their agreement with the insurer, and the individual is not responsible for the difference.

4. "Applied to Deductible." Many health plans require members to pay out a certain amount of money, a “deductible,” before the insurance will begin paying, Palmer says. If the individual has not met the deductible and has to pay for these medical services, the amount that is being applied toward his or her deductible would be in this column. But the Affordable Care Act mandates that some services are provided outside the deductible, at no cost to patients. These services include some cancer screening tests, such as a mammogram. In this EOB, we see that the patient has no amount applied to deductible.

But even if the service is being applied to the deductible, Palmer says that the amount that goes in the “applied to deductible” column will be the lesser, agreed-upon amount — not the higher, original amount that the provider billed.

5. "Coinsurance, Copayment Amount." This may vary depending on what health insurance you have. Sometimes, members must make a copay for an office visit, for example. That is a flat fee. Other services may require coinsurance, a percentage of the cost of the service. If the member on this EOB had been required to pay a copay or a coinsurance for the service, the amount would be listed here.

6."Claims Payment." The amounts in this column break down what the insurance company paid to the provider for each service, with a total at the bottom.

7. Palmer says this is an important part of this EOB. In this case, it’s the insurance company telling the member that it is not his or her responsibility to pay the difference in price between the agreed-upon charges for these services and the amount the provider billed. “It’s very easy to read this [as], ‘It is your responsibility to pay $104’ — somebody could misread it and think they owe $104.15,” Palmer says. “That word ‘not’ should be bold or stand out a lot more.” On some EOBs, Palmer says there is an additional line that says what the patient’s payment responsibility is; in this case, it would list it as $0.

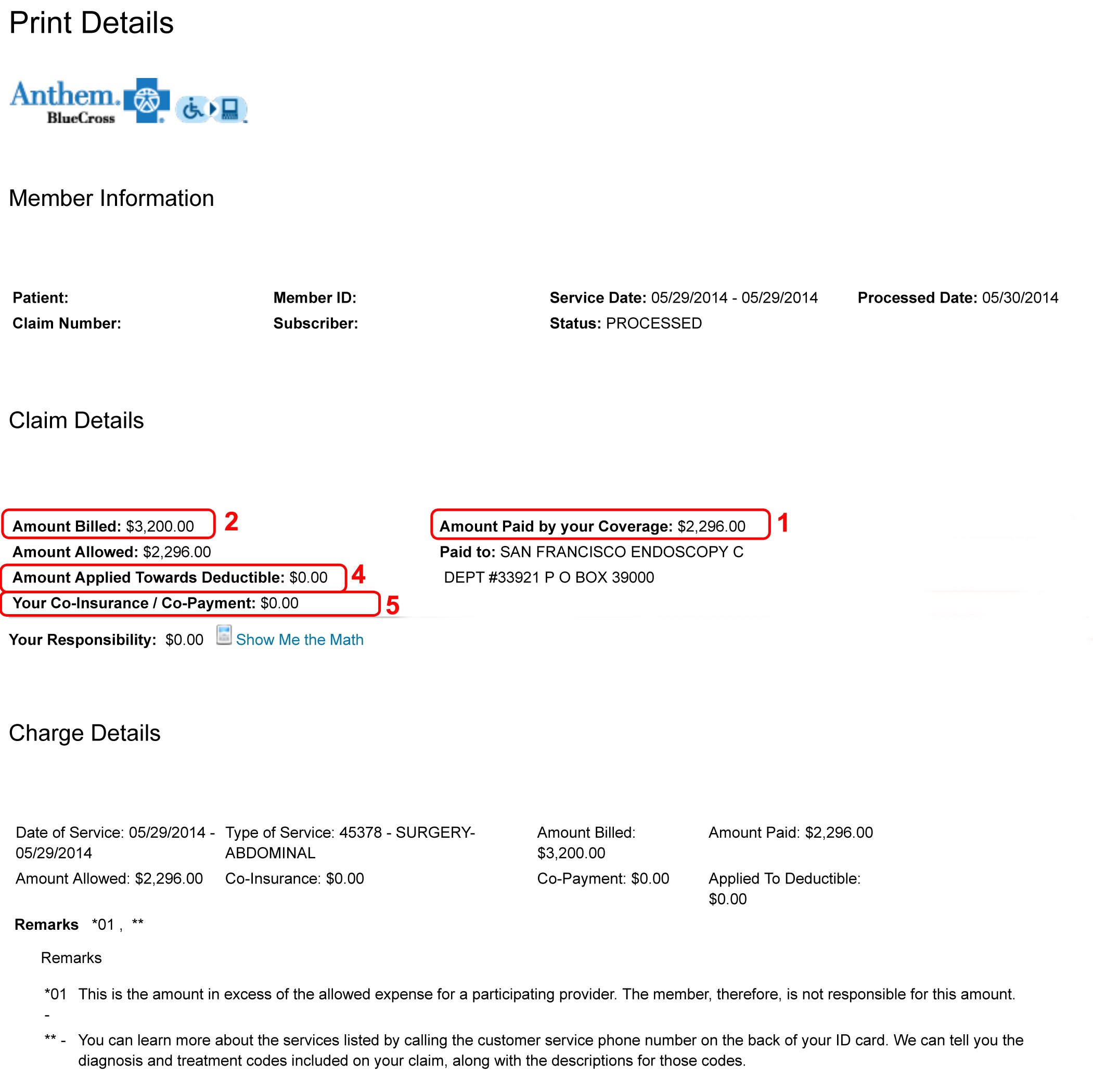

But your EOB might look different from the example above. Or a mailed EOB may look different from what you see online. The above example is a mailed EOB from Anthem Blue Cross, a major health insurer in California. Below is an online EOB, which is also from Anthem Blue Cross, yet it looks quite different. (The numbers in the EOB below line up with the explanations we've provided.)

Numbers 1, 2, 4 and 5 line up with explanations we have provided. But there are no terms on this EOB that line up with 3, 6 and 7 above. Yes, we know this is confusing.

An Explanation of Benefits from Anthem Blue Cross, retrieved online.

Other things Palmer suggests paying attention to on an EOB:

• Look at the “provider of services” and “place of service,” listed on the first EOB in this post as “Mills Hospital” and “outpatient.” Palmer says insurance companies often pay a different rate depending on whether the service was provided in an inpatient setting, outpatient setting or a doctor’s office. “The insurance company is the one that wrote this up, and they may have miscoded the place of service,” Palmer says. “When they do, it will vary on how much your plan pays and how much you’re responsible for.”

• Look for a CPT code (Current Procedural Terminology). CPT codes were developed by the American Medical Association and identify the health care service provided. Palmer says that most times, insurance companies print either a “type of service” (as is listed on the first EOB) or a CPT code. And Palmer says having one, but not both, makes it a bit more difficult to determine if the provider is billing for the right services. Note that the online EOB above does list both a CPT code and a procedure code.

Palmer gives the example of a chest x-ray. If “type of service” is listed as chest x-ray, the individual can’t tell if the charge is for one view or three views, and the price will differ depending. Palmer says it’s often a good idea to call the insurance company to get the CPT code. If the CPT code is written on your EOB, instead of a description of service, Palmer says it’s easy to Google that code and see if it matches up with the service you received.

• Pay close attention to the message or comment box, Palmer says, and be sure you understand why a certain amount is not payable. If an insurance company says something is not payable, it could be a non-covered service that the individual is responsible for. Or, it could be a charge above what the provider and insurer agreed upon, meaning the individual does not have to pay. “Knowing that reason tells you whether you are responsible or not responsible for it,” Palmer says.

• Double-check the calculations on the EOB. Know the benefits that are part of your plan, Palmer says, and keep track of any payments you’ve made toward a deductible. Know where you are in your progress of meeting your deductible and when the insurance company is supposed to start paying.

If you scour your EOB and you do find an error, Palmer says you should determine who made the error -- the provider or the insurer -- and then follow up with them to correct the error.

Sponsored

Finding and correcting an error on an EOB may mean that you, as the individual member, aren’t overcharged, Palmer says. But it also may mean that the insurance company isn’t overcharged by the provider. While our natural instinct may not be to save a health insurance company some money, Palmer says that insurance companies will make profits regardless — so expensive errors only translate to higher premiums passed on to members down the road.

lower waypointnext waypoint

window.__IS_SSR__=true