So, basically, to put it into first-grade math terms: (D)eficit = (S)pending - (R)evenue

Debt - as many college students are all too familiar with - is the amount you owe someone else. The U.S. government has racked up a lot of it over the years in order to pay for all of its programs and services - more than $16.6 trillion, or roughly $52,000 for every American. The debt limit or debt ceiling is the threshold for how much the government can borrow to meet its spending obligations (this sets the limit for how deep into debt American can slide).

Over the years, as the national debt has grown, the Treasury has periodically bumped up against this ceiling. As required by the Constitution, Congress must then approve raising that limit so the government can continue paying for stuff. Although never a particularly popular thing to do, Congress has agreed to raise this limit dozens of time with little fanfare (until recently). Because if the ceiling is not raised, than the U.S. would have to default on its debt. And that would be really bad news.

One way of making some sense of all this stuff is thinking about your own credit card account:

Let's say you want to buy a new big flat screen TV that costs $2,000, but you only have $1,000 in your bank account. In other words, you have a deficit of a grand.

So, \what are you gonna do?

Well, while prudence might suggest saving up until you have enough dough to actually pay for the TV upfront, instant gratification suggests otherwise. So you reach for your credit card and charge it. That is, you pay for it with money you don't actually have: you make the conscious choice to hold onto the $1,000 in your pocket - which you need to pay for your other expenses - and agree to go $2,000 into debt to get the what you want right now.

But before you stepped into the electronics store, you had set your debt ceiling at only $1,000 - the most you ever intended to owe anyone at any given time. But now, since you're borrowing $2,000, you're actually raising your debt ceiling to pay for something that barely fits in your living room.

Of course, the credit card company isn't lending you this money out of the kindness of its heart - it's making a profit by charging you interest. A whole lot it. And the longer you take the pay off the debt, the more interest you rack up.

So, whereas that TV would have cost a cool $2,000 if you had the money to pay for it when you bought it, it's now costing you a good deal more since you're paying off not only the initial cost ($2,000), but also the interest (whatever huge percentage the credit card company is charging you). In other words, the longer you take to pay off the TV, the more debt you accumulate, and the more that TV costs in the long run.

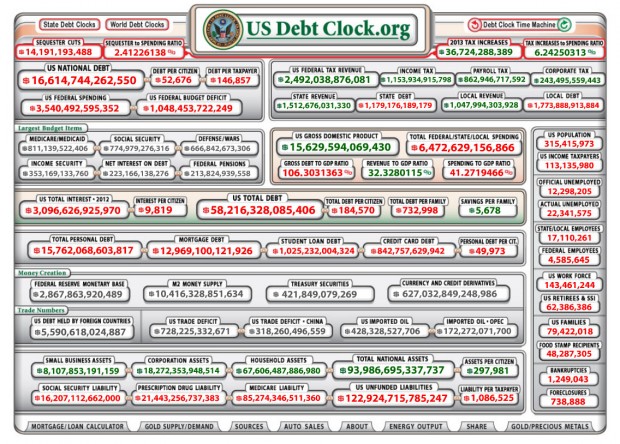

To get a sense of just how fast the U.S. accumulates debt, check out this crrazy real time debt clock (click on the image below).